Видео с ютуба Derivative Pricing

CFA Level I Derivatives - Derivative Pricing and Replication

Derivatives Trading Explained

The Mathematics of Option Pricing from a Quant

17. Options Markets

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

The Trillion Dollar Equation

20. Option Price and Probability Duality

Basics of Derivative Pricing and Valuation (2025 Level I CFA® Exam – Derivative – Module 2)

What is the Monte Carlo method? | Monte Carlo Simulation in Finance | Pricing Options

Binomial Options Pricing Model Explained

Модель Блэка-Шоулза ИНТУИТИВНО объяснена для трейдеров опционов

The Greeks - Stock Option Price Factors Explained

CFA Level I Derivatives - Binomial Model for Pricing Options

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

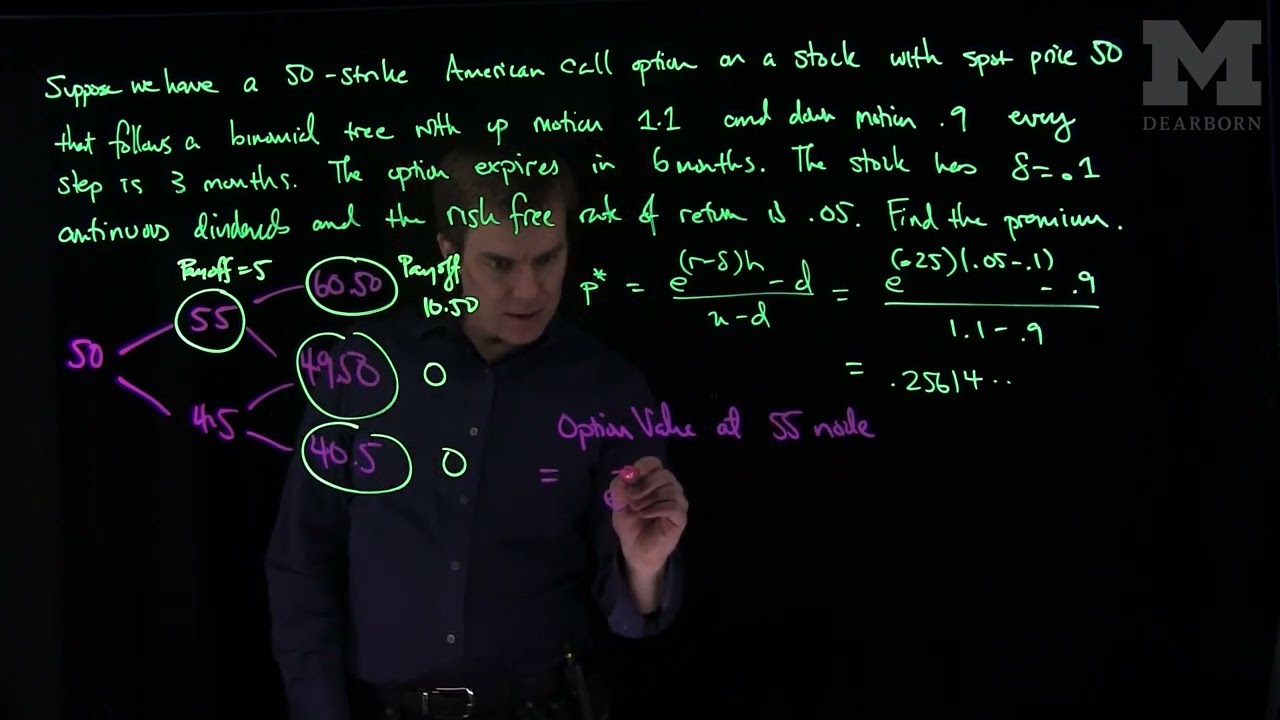

Pricing an American Option: An Example

Quant объясняет ценообразование опционов в условиях нейтральности к риску.

Finite Differences Option Pricing for Quant Finance

Derivative Pricing Models The Formula That Rewrote Finance

Arbitrage, Replication, Cost of Carry – Module 4 Derivatives –CFA® Level I 2026

Monte Carlo Simulation and Black-Scholes for Pricing Options